How to Build a DSA Incentive Programme That Drives Loan Disbursement Without Creating Compliance Risk

Sign up for our newsletter for trending top content!

Introduction

Financial institutions rely heavily on Direct Selling Agents (DSAs) to scale customer acquisition, especially across retail lending, insurance distribution, and fintech partnerships. Yet incentive design remains a major operational blind spot.

Deloitte reports that incentive misalignment and weak governance structures frequently contribute to conduct risk and sales quality issues across financial services distribution networks. At the same time, McKinsey highlights that sales organisations with transparent performance systems consistently outperform peers on productivity and retention.

For Sales Leaders in BFSI and fintech, the challenge is clear. Drive loan disbursement growth without creating mis-selling exposure, payout disputes, compliance breaches, or channel attrition.

This article explains how to design a DSA incentive programme that balances growth with governance. It covers regulatory boundaries, incentive structures, clawback management, transparency expectations, and what automated programme execution should look like in practice.

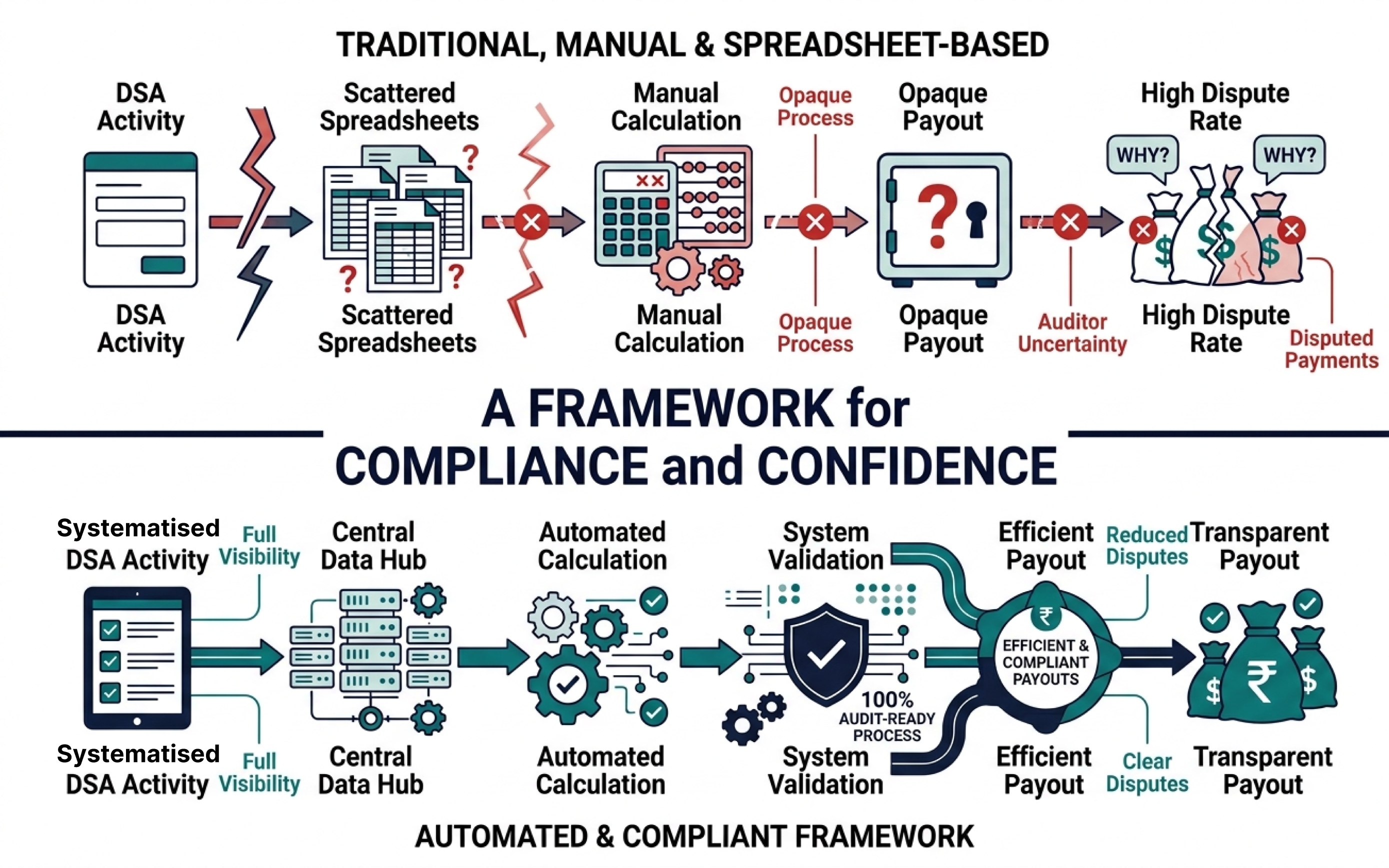

Why Most DSA Incentive Programmes Create More Problems Than They Solve

Many DSA incentive structures optimise for one metric only: disbursement volume. That approach creates short term wins but introduces long term risk.

McKinsey research on sales performance transformation shows that organisations that focus purely on output metrics often experience declining quality outcomes because incentives fail to account for customer value, retention, and compliance behaviour. In BFSI environments, this translates into higher rejection rates, policy lapses, customer complaints, and regulatory exposure.

Common failures include:

Hidden cost: DSA switching behaviour

Transparency often matters more than payout amount. Gartner research on sales incentive effectiveness shows that unclear earnings processes reduce seller trust and increase channel movement.

DSAs regularly move between principals when they cannot understand:

- How incentives were calculated

- Why deductions occurred

- When payouts will arrive

- Which milestones drive higher earnings

Sales Leaders therefore face a dual challenge. They must create incentives that accelerate acquisition while protecting customer outcomes and maintaining distributor confidence.

A structured platform approach becomes essential once DSA networks expand across geographies, products, and payout models.

The RBI and IRDAI Compliance Boundaries Every DSA Programme Must Respect

Regulated industries cannot treat incentives as purely commercial tools.

The Reserve Bank of India (RBI) requires lenders to maintain accountability for outsourced sales activities, including DSA conduct, customer treatment, and grievance handling. RBI outsourcing guidance places responsibility squarely on regulated entities even when third parties originate business.

Similarly, IRDAI distribution regulations emphasise fair selling practices, transparency, and customer suitability.

Sales Leaders should evaluate incentive plans against four compliance boundaries:

1. Avoid behaviour that rewards mis selling

Deloitte conduct risk research shows incentive structures remain one of the strongest predictors of misconduct events in financial services.

Rewarding approvals alone can encourage:

- Product pushing

- Incomplete disclosures

- Aggressive sourcing

- Unsuitable policy recommendations

2. Separate quality from quantity metrics

Aberdeen Group found organisations using balanced performance scorecards achieved stronger sales outcomes than those relying only on output measures.

Recommended weighting:

3. Maintain audit trails

Every incentive calculation should remain traceable.

Salesforce State of Sales research notes that visibility and reporting capabilities increasingly determine operational confidence in sales ecosystems.

4. Define clawback triggers upfront

Unclear deduction logic creates disputes later.

Document lapse conditions, cancellations, fraud triggers, reversals, and timelines before launch.

Designing Incentive Rules That Reward Volume Without Encouraging Mis selling

High performing DSA networks reward behaviour, not just output.

Bain research consistently links customer centric sales behaviour with stronger long term growth and retention outcomes. That matters in lending and insurance because poor customer experiences directly affect portfolio quality.

A practical DSA incentive framework

Use three incentive layers:

Base layer: Production incentives

Reward approved applications and disbursement milestones.

Example:

- Tier 1: Base payout up to threshold

- Tier 2: Accelerator above target

- Tier 3: Quarterly achievement bonus

Quality layer: Behaviour safeguards

Add modifiers linked to:

- Persistency

- Complaint rates

- Documentation accuracy

- Verification success

Strategic layer: Long term retention rewards

McKinsey notes that organisations increasingly shift variable pay towards sustainable outcomes rather than transaction counts.

Examples:

- Retention bonuses

- Cross product incentives

- Customer activation rewards

This is where automation becomes critical.

Platforms such as Paytives allow BFSI teams to configure multi tier incentive logic, track partner performance in real time, automate calculations, and support complex payout structures across regions and currencies.

Explore how Paytives supports BFSI incentive ecosystems here: Paytives for BFSI and Fintech

Real Time Earnings Visibility: Why DSAs Switch Principals for Transparency Alone

Compensation opacity creates channel instability.

Mercer research on incentive effectiveness found that employees and channel participants strongly associate visibility with trust and engagement. When earnings remain unclear, perceived fairness falls sharply.

For DSAs, visibility means immediate answers:

- What have I earned?

- Which deals qualify?

- What deductions apply?

- What target remains?

Without these answers, competitors gain an advantage.

What DSAs expect now

Gartner sales operations studies show sellers increasingly prioritise operational simplicity and visibility over incremental compensation gains.

Paytives addresses this through:

- Real time partner performance tracking

- Automated incentive calculations

- Multi tier partner structures

- White labelled portals

- Global payout capability

Related reading: Channel Partner Incentive Solutions by Paytives

Transparency no longer acts as an operational improvement. It has become a retention strategy.

How to Handle Clawbacks and Lapse Deductions Without Destroying Agent Relationships

Clawbacks remain one of the biggest friction points in DSA ecosystems.

The issue is not deduction itself. The issue is surprise.

Gallup research shows perceived unfairness significantly affects engagement, trust, and retention behaviours. Unexpected deductions damage channel relationships faster than lower payouts.

Build clawbacks around visibility and rules

Recommended structure:

Define triggers explicitly

Common triggers include:

- Loan cancellation

- Early closure

- Policy lapse

- Fraud detection

- Documentation failures

Avoid retrospective rule changes.

Forrester research repeatedly identifies transparency as a leading driver of ecosystem trust.

Automation also reduces conflict.

Instead of spreadsheets and manual reconciliation, systems should automatically apply:

- Eligibility rules

- Deduction logic

- Threshold checks

- Exception handling

Sales Leaders protect relationships when they remove ambiguity from the process.

What a Compliant, Automated DSA Incentive Programme Looks Like in Practice

Modern DSA incentive management combines governance, transparency, and automation.

NASSCOM research on digital transformation highlights automation as a major driver of operational scale within financial ecosystems.

A mature DSA programme typically includes:

Incentive engine

Configure:

- Multi product plans

- Tiered commissions

- Volume accelerators

- Quality modifiers

Compliance layer

Track:

- Audit trails

- Approval workflows

- Rule histories

- Deduction logic

Partner experience layer

Provide:

- Self service dashboards

- Leaderboards

- Earnings visibility

- Mobile access

Execution layer

Integrate with:

- CRM systems

- ERP environments

- Payout infrastructure

Paytives brings these layers together through automated incentive design, real time tracking, multi currency payouts, CRM integrations, and branded partner portals across distributed channel ecosystems.

For BFSI Sales Leaders, automation reduces compliance risk while increasing channel confidence.

Frequently Asked Questions

What is DSA incentive programme management in India?

DSA incentive programme management refers to designing, tracking, calculating, and paying incentives for Direct Selling Agents involved in loan sourcing, insurance distribution, and financial product acquisition. It includes payout rules, compliance controls, clawbacks, performance tracking, and reporting.

How can banks avoid compliance risk in DSA incentives?

Banks should balance volume metrics with quality indicators such as persistency, complaint rates, documentation accuracy, and customer outcomes. RBI outsourcing expectations also require strong oversight and auditability.

Why do DSAs switch principals frequently?

Transparency often drives switching behaviour. Delayed payouts, unclear calculations, and unexplained deductions reduce trust. Real time visibility improves retention and programme engagement.

Can Paytives automate DSA incentive payouts?

Yes. Paytives supports automated incentive calculations, multi tier partner structures, real time tracking, global payouts, and audit visibility for BFSI incentive ecosystems.

Conclusion

Strong DSA incentive programmes do more than increase disbursement volume. They protect compliance, improve transparency, reduce disputes, and strengthen partner relationships.

The next phase of BFSI incentive management will move towards automated, auditable, and real time ecosystems where governance and growth operate together.

Organisations that modernise now will scale faster without increasing operational risk.

See how Paytives automates compliant DSA incentive payouts for BFSI businesses:https://www.therewardstore.com/paytives/solutions/bfsi-fintech

Sign up for our newsletter for trending top content!