How to Design a Credit Card Loyalty Programme That Increases Spend Frequency and Reduces Churn in 2026

Sign up for our newsletter for trending top content!

Introduction

Acquiring a new banking customer can cost five to seven times more than retaining an existing one, according to research from Bain & Company. Bain also found that increasing customer retention by just 5% can raise profits by 25% to 95%. For credit card issuers operating in India's increasingly competitive financial ecosystem, loyalty has become a growth engine rather than a marketing add-on.

Yet many card programmes still focus on rewarding spending volume without influencing behaviour that improves long term profitability, engagement or share of wallet. Marketing leaders face growing pressure to increase transaction frequency, reduce inactivity and build stronger emotional relationships with cardholders.

This article explores how to design a credit card loyalty programme for 2026 that drives meaningful behaviour change. It examines earning structures, tier strategies, redemption experiences, behavioural engagement tactics and emerging consumer preferences shaping loyalty in India's BFSI sector.

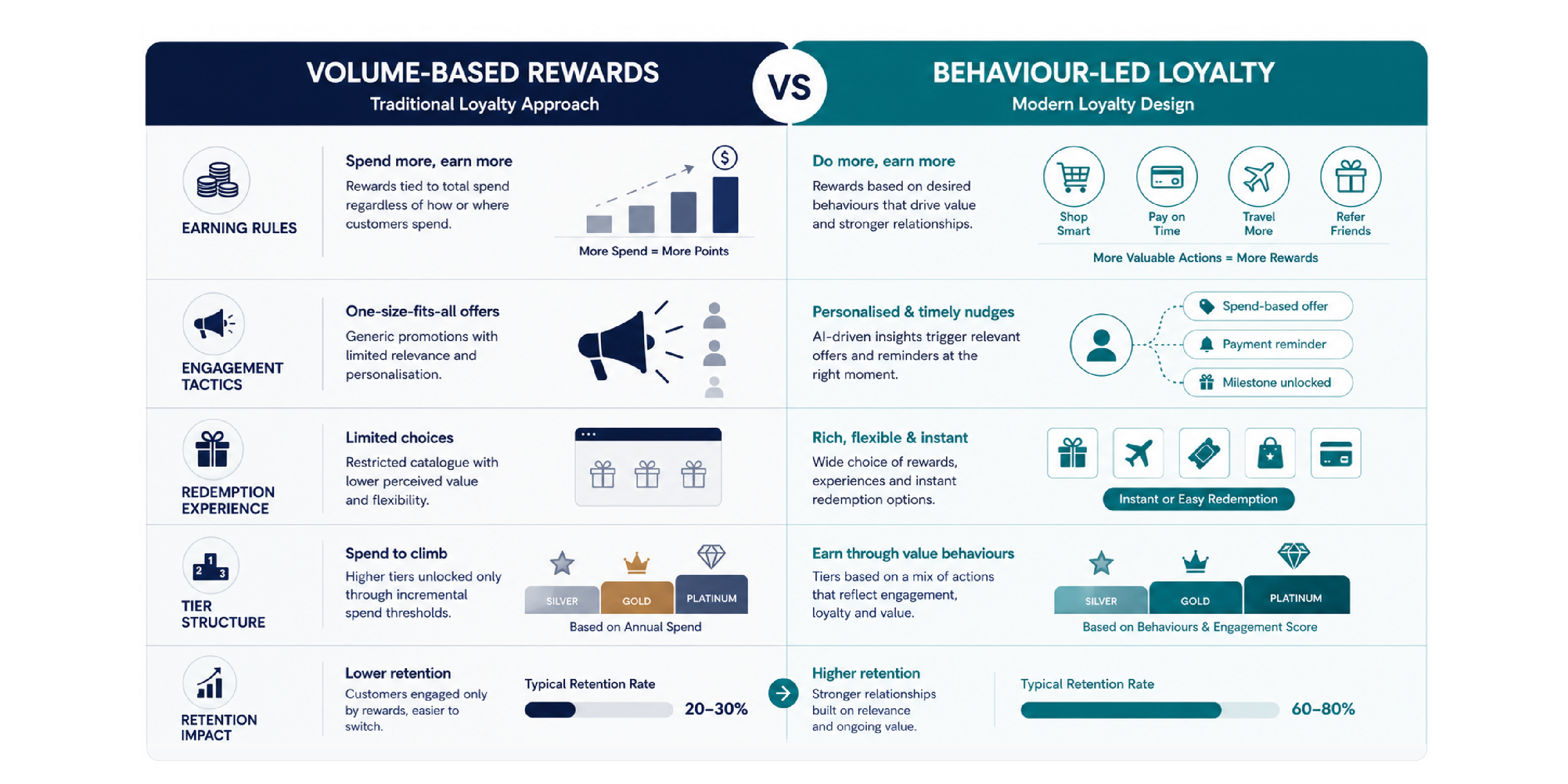

Why Most Credit Card Loyalty Programmes Reward Volume Without Changing Cardholder Behaviour

Many credit card loyalty initiatives assume that offering points for transactions automatically increases engagement. Evidence suggests otherwise.

According to Deloitte, customers increasingly expect loyalty programmes to feel personalised, relevant and contextual rather than transactional. Programmes that reward indiscriminate spending often fail to influence habits because they do not align incentives with desired behaviours.

McKinsey research shows that companies using behavioural personalisation can generate significantly higher engagement and customer satisfaction outcomes. The implication for financial institutions is clear: loyalty architecture should encourage incremental behaviour rather than simply recognise existing spending patterns.

Loyalty should shape behaviour, not simply reward it

Marketing leaders should identify specific behavioural objectives before designing programme mechanics.

These objectives may include:

- Increasing monthly transaction frequency

- Growing wallet share

- Encouraging digital payments adoption

- Expanding usage within targeted merchant categories

- Reactivating dormant customers

- Increasing average tenure

A customer who spends ₹50,000 monthly on routine transactions may already be highly engaged. Offering more points for the same behaviour often delivers limited incremental value.

Instead, institutions should incentivise actions such as:

- First travel booking

- Recurring bill payments

- Increased weekend spending

- New category exploration

- Consecutive months of activity

Forrester research highlights that successful loyalty ecosystems combine emotional engagement, behavioural incentives and perceived exclusivity. Programmes that connect rewards with progress and recognition often sustain engagement more effectively than purely transactional models.

For banks seeking stronger customer lifetime value metrics, loyalty design must evolve from a spend reimbursement mechanism into a behavioural change framework.

The Spend Category Strategy: How to Design Earning Rules That Drive the Transactions You Want

Credit card economics depend heavily on transaction mix. Not all spending categories contribute equally to profitability, retention or strategic objectives.

According to Gartner, customers respond more positively when incentives reflect their lifestyle priorities rather than generic earn rates. Meanwhile, McKinsey reports that personalised experiences can increase customer engagement by as much as 20%.

Designing category-led earning structures

Instead of providing flat rewards across all transactions, banks should prioritise categories that align with growth goals.

Examples include:

- Travel bookings

- Dining experiences

- Utility payments

- Digital subscriptions

- Insurance premiums

- Lifestyle purchases

Example decision framework

Behavioural economists have consistently demonstrated the impact of variable rewards and milestone achievement. Research cited by Deloitte suggests customers engage more actively when they perceive progression and advancement.

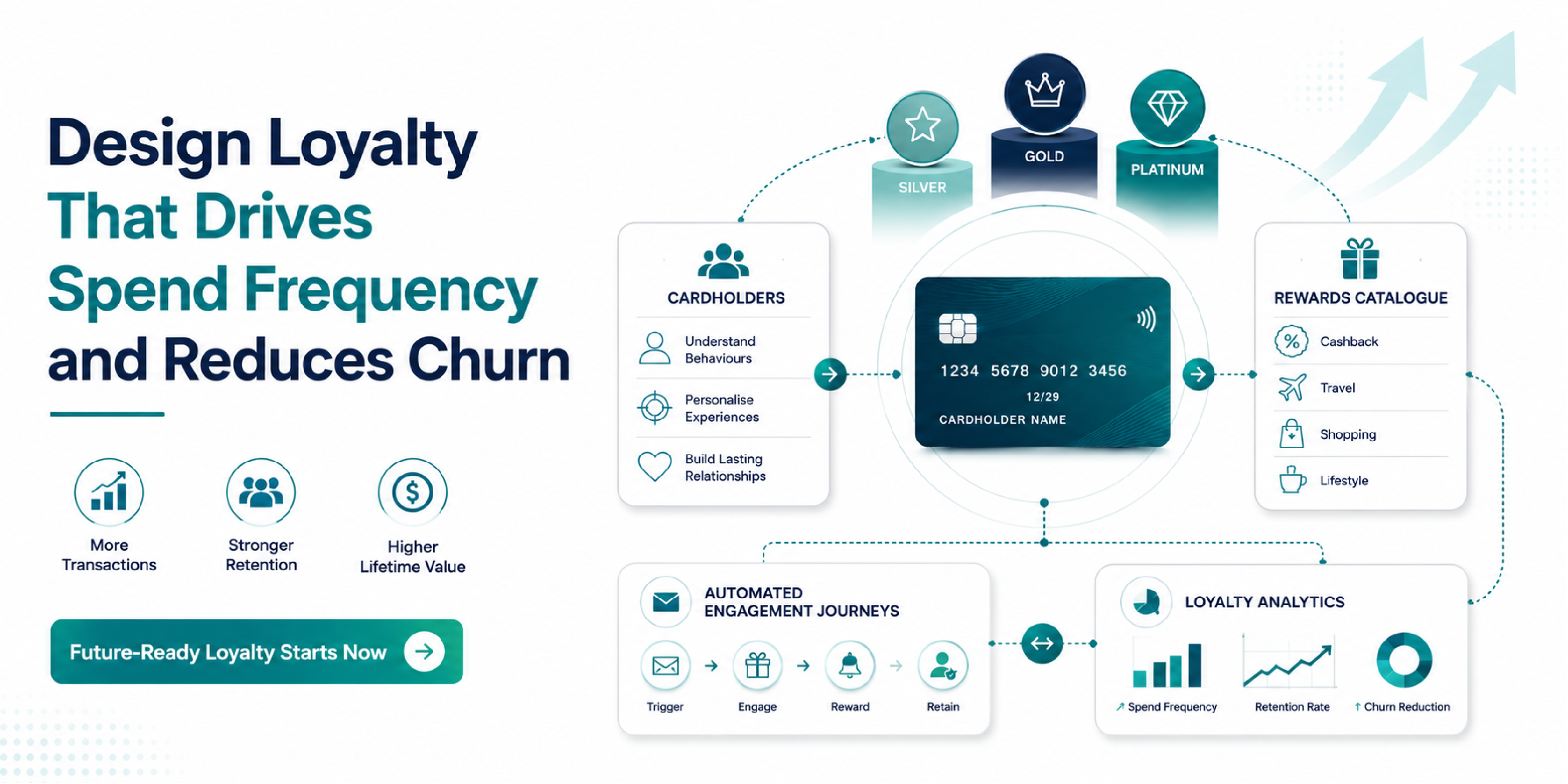

This is where loyalty orchestration platforms become increasingly important. Solutions such as Rekyndl enable financial institutions to build flexible earning rules, segment cardholders dynamically and launch targeted reward campaigns without lengthy development cycles.

Banks can experiment with earning structures, analyse transaction patterns and optimise engagement strategies continuously instead of relying on annual programme redesigns.

For additional insights into loyalty strategy design, explore: https://www.therewardstore.com/blogs

Tier Architecture for Credit Cards: How Many Tiers, What Benefits, and What Switching Costs

Tiered loyalty remains one of the most effective mechanisms for increasing retention because it introduces psychological investment.

Research from Bain & Company indicates that customers who perceive status within a relationship demonstrate higher levels of advocacy and repeat engagement.

Similarly, Gallup has found that emotional attachment strongly correlates with greater customer value and lower attrition.

How many tiers should a credit card programme have?

Most successful financial loyalty programmes operate with three to four tiers.

Too few tiers reduce aspirational motivation. Too many tiers create complexity and weaken progression signals.

A practical framework looks like this:

Entry Tier

Objectives:

- Encourage onboarding

- Establish habits

- Introduce programme value

Benefits:

- Standard earning rates

- Basic redemption access

- Welcome milestone rewards

Growth Tier

Objectives:

- Increase frequency

- Expand wallet share

Benefits:

- Accelerated earning opportunities

- Priority customer service

- Enhanced experiential benefits

Premium Tier

Objectives:

- Retain high-value customer

- Reduce switching risk

Benefits:

- Exclusive experiences

- Concierge services

- Priority redemptions

- Limited access events

The importance of switching costs

Switching costs extend beyond fees or contracts.

Deloitte research suggests customers remain loyal when they accumulate meaningful status, personalised benefits and long-term recognition.

Marketing leaders should ask:

- What would customers lose by moving to another issuer?

- How visible is their progress?

- How quickly can status be achieved?

- Do benefits become more meaningful over time?

Programmes that combine status recognition with curated rewards often create stronger emotional connections than programmes centred solely on cashback.

The future of card loyalty increasingly depends on creating ecosystems customers do not want to leave.

How Redemption Experience Determines Whether Cardholders Actually Value Your Programme

Redemption remains one of the biggest disconnects in loyalty strategy.

Many institutions focus heavily on earn mechanics while underinvesting in redemption journeys. Yet redemption often represents the moment when customers determine whether a programme feels rewarding.

According to Forrester, perceived ease of use significantly influences customer satisfaction and loyalty outcomes. Gartner research similarly shows customers expect immediate, flexible and relevant reward experiences.

Why redemption simplicity matters

Customers lose interest when redemption becomes difficult.

Common friction points include:

- Limited choices

- Complicated rules

- Long processing times

- Poor mobile experiences

- Restricted availability

By contrast, high-performing programmes provide:

- Flexible redemption options

- Digital-first experiences

- Real-time fulfilment

- Personalised recommendations

- Transparent point values

Research from Deloitte indicates consumers increasingly favour experiential rewards and lifestyle benefits over purely transactional incentives.

For credit card issuers, this means offering broader redemption ecosystems that align with customer aspirations.

Examples include:

- Flight bookings

- Hotel bookings

- Dining experiences

- Sports and entertainment access

- Concierge services

- Merchandise rewards

- Gift cards from 5,000+ brands

Rekyndl addresses this challenge by providing an integrated redemption storefront supported by automated campaigns, customer segmentation capabilities and personalised engagement journeys. Financial institutions can deliver relevant reward experiences while maintaining a consistent brand identity.

Ultimately, loyalty succeeds when customers can easily convert effort into meaningful value.

Using Behavioural Triggers to Re-engage Dormant Cardholders Without Discounting

Dormancy presents a significant challenge for card issuers.

According to McKinsey, organisations that effectively use customer data and behavioural insights outperform peers in engagement and retention. Meanwhile, Gartner highlights that contextual interactions produce stronger response rates than broad-based campaigns.

Behavioural triggers outperform blanket promotions

Rather than offering broad discounts to inactive users, marketing leaders should activate personalised interventions.

Examples include:

Milestone reminders

"Complete two transactions this month to unlock bonus rewards."

Status preservation campaigns

"You are 10% away from maintaining your current tier."

Category-based prompts

"Earn accelerated rewards on travel bookings this weekend."

Anniversary recognition

Celebrate tenure milestones with exclusive benefits.

Redemption nudges

Highlight available rewards balances before points expire.

Behavioural science principles such as loss aversion and goal gradient effects influence consumer decision making significantly.

Deloitte research indicates consumers are more likely to respond when messaging emphasises preserving benefits rather than earning entirely new rewards.

Platforms designed for modern loyalty execution increasingly embed these capabilities directly within marketing workflows.

With Rekyndl, banks can create automated journeys for onboarding, inactivity management, milestone engagement and win-back campaigns across email, SMS, push notifications and in-app channels.

Instead of relying on costly discount campaigns, financial institutions can build engagement loops that encourage sustained card usage and improve long-term profitability.

What Indian Cardholders in 2026 Want From Loyalty: The Data Behind Shifting Reward Preferences

Indian consumers continue to redefine expectations around financial loyalty.

Deloitte's consumer insights research suggests modern customers increasingly value flexibility, relevance and personalisation over one-size-fits-all incentives.

Meanwhile, McKinsey notes that younger customer segments expect loyalty ecosystems to function more like digital experiences than traditional points schemes.

Emerging expectations shaping loyalty in 2026

Several trends are becoming increasingly important.

Instant gratification

Consumers expect immediate rewards and real-time visibility into programme benefits.

Lifestyle integration

Cardholders increasingly prefer rewards that connect with travel, entertainment, wellness and experiences.

Personalisation

Generic offers no longer resonate. Customers expect programmes to understand preferences and spending patterns.

Choice

Research from Forrester indicates consumers appreciate flexibility in how they earn and redeem rewards.

Recognition

Status and exclusivity continue to influence loyalty decisions, particularly among affluent segments.

Loyalty preferences expected to grow

For marketing leaders in BFSI and fintech organisations, loyalty increasingly represents a customer experience strategy rather than a promotional initiative.

The institutions that adapt fastest will likely strengthen engagement, increase transaction frequency and defend market share more effectively over the next decade.

Frequently Asked Questions

What makes a successful credit card loyalty programme in India?

Successful programmes encourage behaviours that improve long-term customer value rather than simply rewarding existing spending. They combine targeted earning rules, meaningful redemption options, personalised engagement and aspirational tiers. Bain & Company research consistently highlights retention as a major driver of profitability. Loyalty initiatives should therefore focus on frequency, tenure and emotional engagement.

How many tiers should a credit card loyalty programme have?

Most effective programmes operate with three or four tiers. This structure creates progression while remaining easy for customers to understand. Too many tiers increase complexity and weaken motivation. Marketing leaders should align tier design with behavioural objectives and customer lifetime value targets.

Why is redemption important in reducing cardholder churn?

Redemption creates the moment when customers experience programme value directly. Complicated redemption journeys often reduce perceived reward value and weaken engagement. Research from Forrester indicates customers respond positively to frictionless experiences that offer flexibility, convenience and choice.

How can banks re-engage inactive credit card users?

Banks should use behavioural triggers such as milestone reminders, status protection campaigns and personalised category offers. Automated journeys often outperform broad discount campaigns because they create relevance and urgency. Rekyndl enables institutions to build these journeys using segmentation, customer data and multi-channel communications.

What trends will shape credit card loyalty in India by 2026?

Personalisation, experiential rewards, real-time engagement and flexible redemption models are expected to become increasingly important. Deloitte and McKinsey research both suggest consumers want loyalty experiences that feel contextual, digital-first and aligned with their lifestyles. Financial brands that respond to these expectations are likely to see stronger retention outcomes.

Conclusion

Credit card loyalty programmes in 2026 must do more than reward spending. They need to shape behaviour, encourage progression and deliver experiences customers genuinely value. Institutions that align earning structures, tier strategies, redemption ecosystems and behavioural engagement tactics will strengthen retention while increasing transaction frequency.

As expectations continue to evolve, loyalty will become a primary differentiator for banks and fintech brands competing for long-term customer relationships.

See how Rekyndl powers credit card loyalty programmes for Indian banks and fintech companies. Book a tailored consultation.

Sign up for our newsletter for trending top content!