What Should a Consumer Loyalty Platform for Indian Banks Do in 2026? A CXO's Evaluation Guide

Sign up for our newsletter for trending top content!

Introduction

McKinsey reports that companies leading in personalisation generate 40% more revenue from those activities than slower-moving peers. In financial services, that finding carries serious implications because loyalty expectations have moved beyond points accumulation to real-time engagement, contextual rewards, and intelligent customer journeys.

Indian banks face rising acquisition costs, increasing digital competition, and customers who switch providers more easily than ever. Bain & Company found that improving customer retention by just 5% can increase profits by 25% to 95%, making loyalty infrastructure a board-level growth decision rather than a marketing initiative.

This guide examines what CXOs should expect from a consumer loyalty platform for banks India 2026, including capability requirements, compliance considerations, marketing automation expectations, and build versus buy economics.

The objective is simple: help banking leaders avoid costly technology decisions while preparing for the next phase of customer engagement.

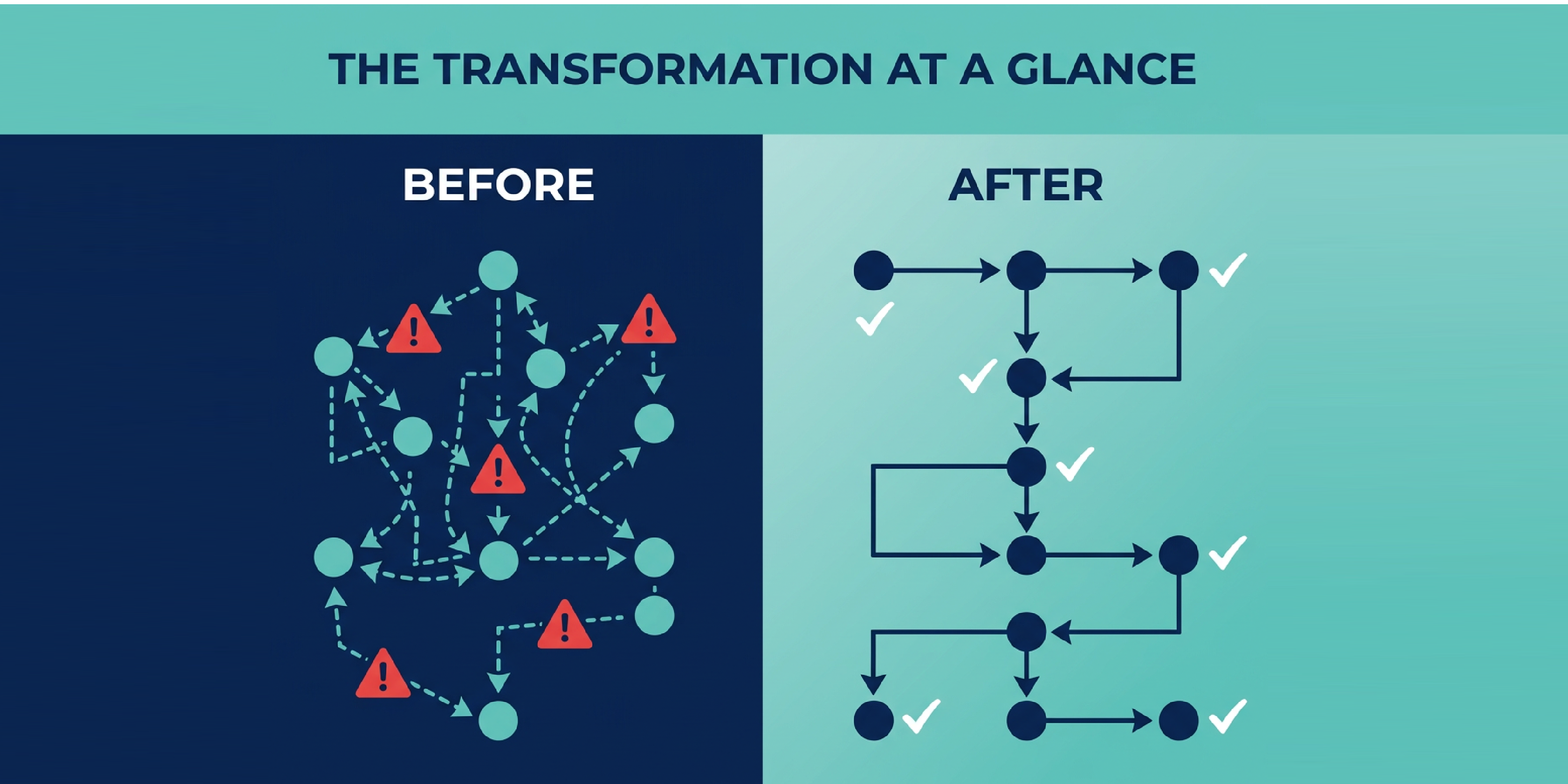

Why Legacy Bank Loyalty Stacks Are Failing the Modern Indian Customer

Traditional banking loyalty systems were built around transaction rewards, periodic campaigns, and siloed points engines. That architecture no longer matches customer behaviour.

Deloitte reports that customers increasingly expect personalised, predictive experiences across channels. Meanwhile, Gartner research shows that organisations relying on fragmented customer systems struggle to deliver consistent engagement journeys.

Legacy stacks operate as disconnected systems

Most mid-tier banks still separate:

• Loyalty engines

• CRM workflows

• Campaign orchestration

• Reward fulfilment

• Customer analytics

This separation creates delays in execution and weakens customer visibility.

For example, a customer completing a high-value transaction may receive recognition days later because campaign systems and loyalty databases remain disconnected. In digital banking, timing affects engagement.

Static loyalty models reduce engagement

Bain research shows emotional loyalty drives stronger retention than purely transactional models. Yet many banking programmes still rely on quarterly campaigns and fixed point accrual structures.

Modern customers increasingly expect:

Platforms such as Rekyndl address this gap by combining loyalty orchestration, segmentation, customer journeys, and redemption infrastructure in one ecosystem instead of layering disconnected tools.

The Five Capabilities a 2026 Banking Loyalty Platform Must Have

CXOs evaluating loyalty platforms should move beyond reward catalogues and assess strategic capabilities.

Forrester notes that customer obsession leaders grow revenue faster because they operationalise customer understanding across systems.

1. Behaviour-based segmentation

Banks need segmentation based on transaction activity, product holdings, lifecycle stage, and engagement signals.

Static demographic targeting no longer produces sufficient engagement.

2. Embedded marketing automation

A loyalty engine without journey orchestration limits programme effectiveness.

Banks should expect:

• Welcome journeys

• Card activation campaigns

• Win-back flows

• Birthday engagement

• Dormancy reactivation sequences

Rekyndl combines loyalty management with automated journey building, reducing operational complexity.

3. Gamification mechanics

Gartner research indicates gamification improves engagement when tied to measurable behaviour.

Banks increasingly adopt:

• Badge systems

• Milestone rewards

• Challenges

• Interactive experiences

4. Integrated redemption storefronts

Customers expect immediate redemption experiences rather than offline fulfilment.

Reward ecosystems should support:

• Travel bookings

• Hotel bookings

• Gift cards from 5,000+ brands

• Dining experiences

• Lifestyle rewards

5. Omnichannel delivery

McKinsey highlights that customers interact across channels continuously.

The platform must orchestrate communication through:

• Email

• SMS

• Push notifications

• In-app experiences

• Branch interactions

Marketing Automation vs Points Engine: Why Banks Need Both in One Platform

Many banks still treat loyalty and marketing automation as separate investments. This creates operational inefficiency.

McKinsey found that personalisation leaders achieve stronger customer acquisition efficiency because they activate data continuously rather than periodically.

A standalone points engine answers only one question:

“What reward should the customer receive?”

Modern banking loyalty must answer:

“What experience should happen next?”

Why orchestration matters

Consider a customer journey:

Customer activates premium card → reaches spending threshold → receives recognition → enters tier upgrade journey → receives experiential offer → reactivates after dormancy.

Without automation, marketing teams manually coordinate campaigns.

With integrated systems, journeys execute automatically.

Rekyndl combines:

• Loyalty programme builder

• Automated journey orchestration

• Customer segmentation

• Redemption experiences

• Multi-channel engagement delivery

This model matters because Deloitte reports organisations using integrated customer platforms achieve stronger engagement consistency.

Operational impact comparison

For banking CXOs, the question is no longer loyalty versus marketing. It is whether both functions operate inside one architecture.

How to Evaluate a Loyalty Platform's Compliance Architecture for RBI Readiness

Compliance architecture will increasingly influence loyalty platform decisions.

Indian banks operate under strict governance expectations covering data handling, auditability, security, customer consent, and operational controls.

Gartner identifies trust and governance as critical selection criteria for customer platforms in regulated industries.

Evaluate these five compliance areas

1. Audit trails

Every customer action, reward event, and campaign execution should maintain traceable logs.

2. Consent management

Banks need transparent customer permission workflows across communication channels.

3. Data segregation

Platforms should support role-based access and controlled visibility.

4. Integration governance

Loyalty systems increasingly integrate with core banking, CRM, and marketing infrastructure.

Controlled API architecture becomes essential.

5. Scalability across geographies

Banks expanding internationally need multi-country reward fulfilment and localisation capabilities.

NASSCOM highlights governance readiness as a growing requirement for financial institutions adopting customer platforms.

Platforms purpose-built for regulated industries increasingly embed compliance architecture alongside engagement functionality.

Banks evaluating providers should include compliance stakeholders from procurement stage rather than post-selection.

The Hidden Cost of Building Loyalty In-House for Mid-Tier Banks

Building internally appears attractive because banks retain ownership. Financially, the equation often changes.

McKinsey research shows large transformation initiatives frequently exceed expected budgets and timelines.

A banking loyalty ecosystem requires:

• Loyalty logic engine

• Customer segmentation layer

• Campaign orchestration

• Reward fulfilment ecosystem

• Analytics stack

• Security controls

• Compliance workflows

• Mobile interfaces

Forrester notes that maintaining customer engagement technology increases operational overhead when organisations manage fragmented architecture.

Cost comparison framework

Mid-tier banks face an additional challenge: talent allocation.

Technology teams already prioritise lending, payments, cybersecurity, and digital banking initiatives.

Building loyalty internally diverts resources from core banking innovation.

This explains why many institutions increasingly adopt configurable platforms rather than bespoke development.

A Decision Framework for Choosing a Consumer Loyalty Platform in 2026

CXOs should evaluate loyalty platforms across business impact, not feature volume.

Bain emphasises that customer retention economics outperform acquisition economics over time.

Use the following framework:

Strategic evaluation criteria

A banking loyalty platform should:

✓ Combine loyalty and engagement orchestration

✓ Reduce operational overhead

✓ Support regulatory expectations

✓ Deliver measurable retention outcomes

✓ Scale internationally

For financial institutions assessing modern customer engagement infrastructure, solutions built specifically for regulated ecosystems such as Rekyndl provide stronger alignment with banking requirements.

Frequently Asked Questions

What should a consumer loyalty platform for Indian banks include in 2026?

Banks should prioritise customer segmentation, marketing automation, omnichannel engagement, integrated rewards, compliance controls, and journey orchestration. Points engines alone no longer satisfy customer expectations. Modern platforms must manage both loyalty logic and engagement execution.

How do banks evaluate loyalty platform compliance readiness?

Banks should assess audit trails, consent management, API governance, access controls, and scalability. Compliance teams should participate early in evaluation because governance requirements affect architecture decisions.

Why is marketing automation important in banking loyalty?

Marketing automation allows banks to trigger contextual experiences automatically. Examples include onboarding journeys, dormancy recovery, milestone engagement, and product activation campaigns. Deloitte identifies personalisation as a key engagement driver.

Can Rekyndl support financial services loyalty programmes?

Rekyndl supports loyalty programme creation, customer segmentation, journey automation, gamification, redemption experiences, and omnichannel engagement. It aligns particularly well with banks seeking one platform for loyalty and customer lifecycle management.

Conclusion

Banking loyalty in 2026 will depend less on points accumulation and more on orchestrated customer experiences. Platforms that combine loyalty management, automation, rewards infrastructure, and governance controls will outperform fragmented systems.

As Indian banks accelerate digital transformation, loyalty platforms will increasingly become retention engines and growth infrastructure rather than campaign tools.

See how Rekyndl is built specifically for the compliance and scale requirements of Indian banks: https://www.therewardstore.com/rekyndl/solutions/financial-services-fintech

Sign up for our newsletter for trending top content!