Build vs buy a loyalty platform: a BFSI decision guide for CXOs

Sign up for our newsletter for trending top content!

Introduction

According to Forrester, banks that deploy purpose-built loyalty platforms see up to 25% higher customer engagement and retention compared to CRM-only solutions. CXOs in BFSI face a critical choice: develop an in-house platform or adopt a commercial solution. Both approaches have trade-offs in cost, time, scalability, and risk.

This guide evaluates the advantages and challenges of building versus buying a loyalty platform, highlights key decision criteria, and provides frameworks for choosing the optimal path. By aligning strategy with operational and financial objectives, BFSI leaders can accelerate loyalty initiatives while maximising ROI and customer lifetime value.

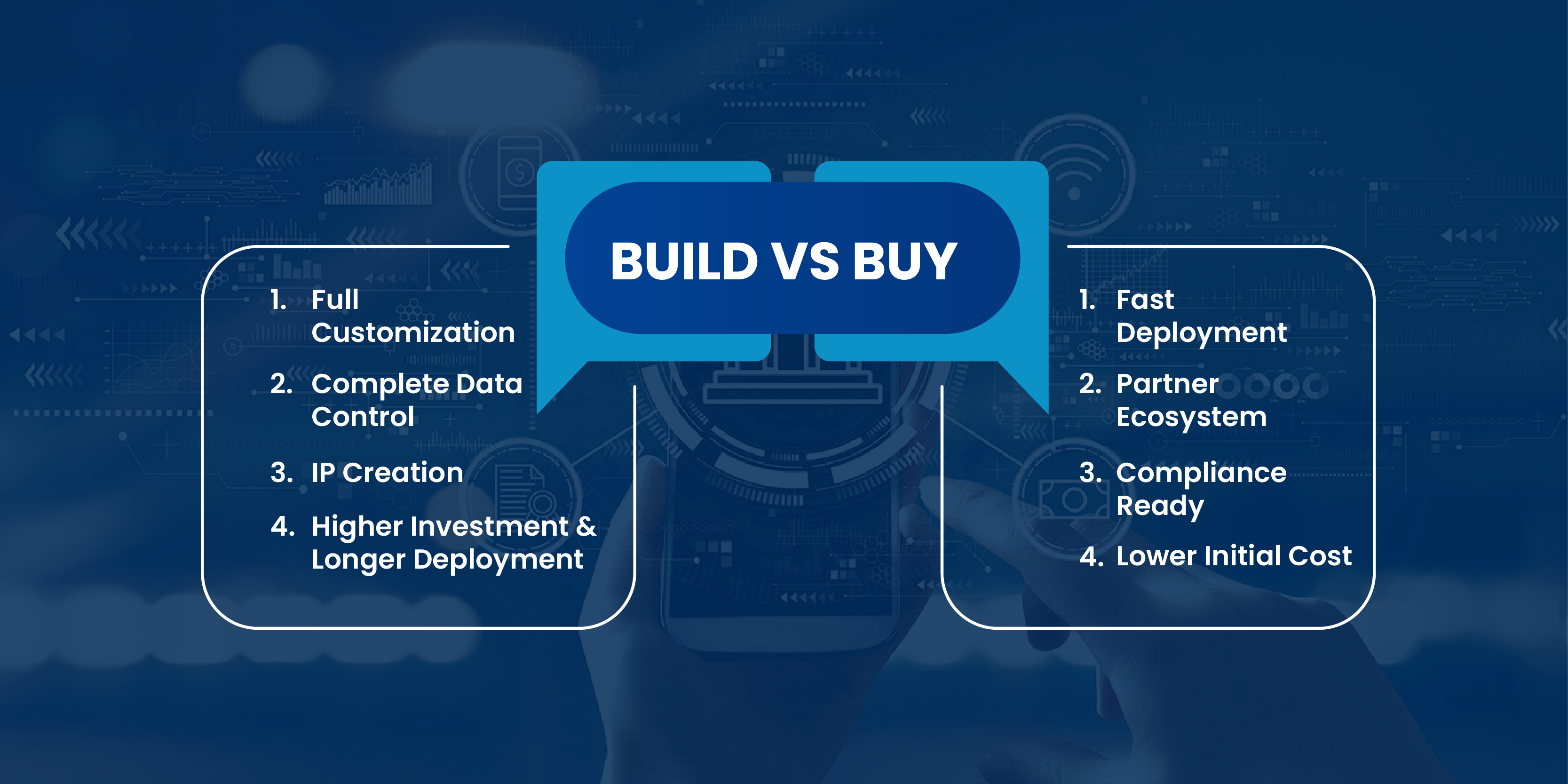

Why do BFSI organisations consider building their own loyalty platforms?

Banks and fintech firms may choose to build an in-house platform for full control over features, custom integrations, and proprietary data management. McKinsey research indicates that custom-built platforms can align tightly with internal workflows and compliance requirements.

Benefits of building:

- Full control over design, data, and workflow

- Ability to integrate proprietary analytics and reporting

- Customisation for unique business models

Challenges:

- High upfront investment and ongoing maintenance costs

- Longer time-to-market (6–12+ months)

- Dependency on IT resources for updates and compliance

Decision guide: Consider internal IT bandwidth, compliance complexity, and long-term strategic priorities before committing to an in-house build.

How does buying a loyalty platform reduce risk and accelerate deployment?

Commercial loyalty platforms provide pre-built features, BFSI-specific integrations, and compliance-ready frameworks. Aberdeen Group notes that organisations adopting SaaS loyalty solutions launch programmes 3–4 times faster than building internally.

Advantages of buying:

- Reduced development cost and faster go-live

- Continuous platform upgrades and support

- Built-in analytics, reward catalogues, and omnichannel capabilities

Comparison

Platforms like Rekyndl offer BFSI-ready modules with pre-configured APIs and analytics, minimising operational risk while delivering measurable engagement results.

What factors should CXOs consider when deciding build vs buy?

Selecting the right approach requires a balanced evaluation of cost, control, speed, and scalability. Deloitte recommends a framework:

Decision Criteria Framework:

- Strategic Alignment: Does the platform support long-term digital transformation goals?

- Resource Availability: Are internal teams capable of building, maintaining, and scaling the system?

- Compliance and Security: Can in-house solutions meet regulatory standards efficiently?

- ROI Analysis: Compare projected incremental revenue and engagement versus investment.

- Market Agility: Will the solution allow rapid adaptation to changing customer expectations?

CXOs should weigh each criterion quantitatively, using scenario analysis to assess potential revenue uplift and operational costs.

How can banks optimise implementation regardless of build or buy?

Best practices include:

- Modular deployment: launch core features first, expand gradually

- Integration planning: ensure APIs connect CRM, core banking, and reward systems

- Data governance: standardise formats and reporting for compliance

- Continuous analytics: measure KPIs such as redemption rates, engagement, and incremental revenue

Real-time dashboards and reporting, as provided by platforms like Rekyndl, allow CXOs to monitor programme performance without heavy IT intervention, ensuring both scalability and agility.

Frequently Asked Questions

When should a bank build vs buy a loyalty platform?

Build when full customisation and proprietary workflows are critical, and IT capacity is sufficient. Buy when speed, lower risk, and compliance-ready solutions are priorities.

What is the total cost of building an in-house platform?

Costs include software development, IT resources, ongoing maintenance, compliance audits, and upgrades, often exceeding six figures for large BFSI organisations.

How long does implementation take for build vs buy?

Building can take 6–12+ months depending on complexity; buying a BFSI-ready SaaS platform can reduce implementation to 6–10 weeks, including integration and testing.

Can Rekyndl help banks deploy loyalty programmes efficiently?

Yes. Rekyndl provides a BFSI-ready loyalty platform with pre-built APIs, reward catalogues, analytics dashboards, and compliance features, enabling faster deployment and measurable engagement outcomes. (Rekyndl BFSI solutions)

Conclusion

CXOs must weigh control, cost, and speed when choosing between building or buying a loyalty platform. Buying a BFSI-ready solution like Rekyndl reduces risk, accelerates deployment, and provides measurable engagement, while building in-house offers total customisation but with higher investment and longer timelines. Aligning platform choice with strategic goals ensures banks maximise customer loyalty, revenue, and operational efficiency.

See how Rekyndl enables banks and fintech organisations to deploy loyalty platforms quickly and effectively, optimising engagement and ROI. Explore the solution today.

https://www.therewardstore.com/rekyndl/solutions/financial-services-fintech

Sign up for our newsletter for trending top content!